Update: New Zealand King Salmon (NZK.NZX, NZK.ASX)

Interim Accounts to 31st July, 2022

Note:

All amounts in New Zealand dollars (NZ$) unless otherwise stated.

New Zealand King Salmon (NZK) made an announcement to the NZX yesterday on its unaudited interim results to 31st July, 2022.

The interim results are condensed and don't provide the detail of the last annual results to 31st January, 2022.

The latest interim results are referred to here as HY23 while last years interim results are named HY22.

New Zealand King Salmon was recently and surprisingly able to raise $60.1m from investors through a rights issue.

Had it not raised a significant amount of money it's likely NZK would not have survived in the medium-term.

Its current business model has been failing mainly as a result of increased sea temperatures which have been causing fish deaths.

Recast Investor’s previous posts on this company can be found in the Interims to 31.7.21, an Alert on 13.4.22, the Annuals to 31.1.22 and a Tradeshot on 22.4.22.

NZK has a planned project called Blue Endeavour which is their proposed solution to changing sea temperatures.

But a government decision on whether the project can go ahead is taking a very long time.

It's hard not to have some sympathy for the company with the endless delays it faces in getting this Blue Endeavour project off the ground.

The company is also an exporter in a country running a large trade deficit.

If the Blue Endeavour project is approved there will need to be another fund-raising process. This issue was not pointed out too strongly (if at all) at the time of the previous rights issue.

The latest six months has been very difficult for the company and its performance is poor.

It has reduced its number of employees significantly.

The company lost a lot of money in this interim period and the funds it raised are disappearing quickly. It did pay off debt however and has an unexercised overdraft facility.

Revenue Snapshot

The fair value increase in biological assets is put above the line in the company's calculation of EBITDA.

EBITDA is not an IFRS measure and for other reasons it is not a metric of value here.

However, EBITDA does have some use in comparing one company to another which is not the present case.

Gain on biological assets is moved down the revenue statement to unrealised items because of its lower quality (unsupported by external accounting transactions).

Freight is also a direct cost and is added to costs of sales rather than itemised separately.

EBIT was similar to PCP (previous comparable period) but there was a massive net loss after tax of $24.5m.

This was caused by a fall in the fair value gains in biological assets which fell to $13.2m from the PCP's $30.7m.

Balance Sheet Snapshot

The balance sheet is shrinking even with the injection of cash from the rights issue. The total assets are $184.8m in HY23 compared to $197.3m for PCP.

The accounts receivable has dropped by a very significant amount and one wonders how this was achieved.

Were receivables factored and if not, how did the company get many customers to pay earlier?

Cash payments to suppliers were also reduced but sales were about the same.

Current biological assets were dramatically more at the end of HY22 ($65.5m) than at balance date in HY23 ($47.6m).

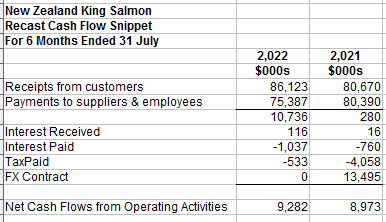

Cash Flow Snapshot

The gap between profit and operating cash flow is large.

The positive operating cash flow was a surprise because there was no similar transaction to the PCP's $13.5m early redemption of forex-related contracts.

This forex transaction lifted the operating cash flow from negative to positive in the PCP.

How did the company lose such a lot of money as shown in the revenue statement but still have a positive operating cash flow?

The operating cash flow is a very important number and goes right to the heart of a company's financial health.

Without a forex contracts’ early redemption transaction the company has used a few methods to create positive operating cash flow.

Significant accounts receivable reductions

Small accounts payable increases

Inventory changes from destocking farms

Capital expenditure (capex) was down quite significantly on the PCP which helped investing cash flow. The cash position at balance date was a healthy $19.8m as a result of cash left over from the rights issue.

Summary

NZK is a business in distress. All its hopes seem to lie in the approval (creates a large intangible) and eventual (not guaranteed) success of the Blue Endeavour project.

Worryingly, a recent The Guardian article dated 26th May, 2022 reported from an interview with the CEO Grant Rosewarne who, perhaps in an unguarded moment, said that, “Even when the fish were towed out to cooler waters, many were dying: 37% in 2022, compared to just 10% in 2018.”

This is indeed a major concern for the Blue Endeavour project.

The eventual outcome of the government’s consideration of the Blue Endeavour project is following its usual glacial decision-making processes and is uncertain.

Another difficulty also looms. Animal rights activists are increasingly vocal about the very high numbers of fish deaths in NZK’s salmon farm operations.

After NZK admitted to a 42% death rate in the warm waters that it farms, SAFE, an animal rights group, were reported as strongly objecting to the way salmon were farmed by NZK. It was also reported in the same article that last summer NZK made “160 trips to the Blenheim landfill to dump 1,269 tonnes of dead salmon”.

SAFE further stated that salmon need to be able to swim to cooler waters in the hotter months which is what they do in the wild.

Pressure from animal rights people will only increase as they lobby for controls under New Zealand’s Animal Welfare Act.

The company has cut its number of staff and is looking at all areas of its business in an effort to reduce costs.

It has fallowed (emptied) pens and changed its breeding programs to reduce fish deaths.

Harvest volumes are down but revenue was similar because of price increases.

The company’s EBIT is a massive -$35.4m if biological asset gains are placed further down the revenue statement which of course brings into question their whole operation.

There has been some talk during the year about a trade sale. The company has subsquently denied that it is for sale.

The cash and cash equivalents of $19.8m at balance date give the company some breathing room for a while.

The high equity to total assets is also a positive given that intangibles are very low and borrowings are reasonably low.

If Blue Endeavour is approved (and there are a lot of jobs and election votes involved) the company will be able to ignite new hope for its investors. But a whole new set of uncertainties (and costs) around developing an untried deepish-water salmon farming operation will emerge.