Update: Retail Food Group (RFG.ASX)

Update: Retail Food Group (RFG.ASX)

Annual Accounts to 1st July, 2022 (Three Year Analysis)

Notes:

All amounts are in Australian dollars (AU$) unless otherwise stated.

Overview

Retail Food Group (RFG) was previously covered in a basic analysis of the annuals to 2nd July, 2021 and an update to the 31st December, 2021.

The company earns revenue from multiple sources including selling goods, selling franchise agreements, selling distribution rights, sub-leasing property in which some franchises operate and other sources such as interest income.

RFG has intellectual property ownership of the Donut King, bb’s café, Brumby’s Bakery, Michel’s Patisserie, Esquires Coffee Houses (Australia & New Zealand), Pizza Capers Gourmet Kitchen, Crust Gourmet Pizza Bar, The Coffee Guy, Café2U and Gloria Jean’s Coffees Brand Systems.

RFG also is involved in the development and/or management of the Donut King, Brumby’s Bakery, Michel’s Patisserie, Esquires Coffee Houses (New Zealand), Pizza Capers Gourmet Kitchen, Crust Gourmet Pizza Bar, The Coffee Guy, Café2U and Gloria Jean’s Coffees Brand Systems throughout the world. In some cases the businesses are directly managed and in others RFG is the licensor.

Lastly, RFG is involved in the development and management of coffee roasting facilities, and the wholesale supply of coffee and allied products to the Group’s Brand Systems and third-party accounts, under the Di Bella Coffee business brand.

RFG has been downsizing and this is reflected in the reduced turnover.

Audit Report

(Annual Report: Notes to the Financial Statements pp. 100-107)

The auditors FY22 were the Australian representatives of the large and well-known firm KPMG which operates internationally. They stated that the accounts show a true and fair view of RFG’s operations at balance date and complied with the Australian Accounting Standards and the Corporations Regulations 2001.

They further stated that their audit was in accordance with Australian Auditing Standards.

However, the auditors identified a few significant issues:

1. Goodwill and other indefinite life intangible assets.

The auditors said that there was a lot of uncertainty around the valuations of goodwill and indefinite life intangible assets because they comprised so much of the total assets on the balance sheet. They were very material and post-Covid-19 there was real difficulty in evaluating the cash flow forecasts used to create the goodwill impairment figures and the goodwill item.

Even small changes in assumptions lead to very different impairment and goodwill figures.

2. Revenue Recognition

The auditors drew attention to some of the complexities of the judgements involving revenue recognition around the sale of franchise agreements. The potential for misstating revenue is significant.

3. Lease accounting with regard to the estimate of lease arrears and assessment of recoverability of finance lease receivables. The auditors stated there was considerable uncertainty surrounding the recoverability of lease arrears.

RFG has an Audit and Risk Management Committee.

Remuneration Sources for KPMG from RFG:

There are significant increases in payments for services other than audit and review services of the financial statements provided by KPMG between FY21 and FY22.

KPMG captures an 80.6% increase in audit and review of other financial statements while tax services increased 68.4% and other services increased 113.8% over the same period but are nevertheless smaller than the core audit services.

Core audit and review services performed by KPMG increased to 0.70% of sales in FY22 from 0.60% of sales in FY21.

Interestingly, KPMG was paid less than half of the FY20 auditor’s remuneration for core audit and review services.

But overall KPMG’s non-audit services such as tax advice income is greater than their income from the core audit function.

This can place an auditor in a difficult position. Strongly challenging directors on audit matters can have the potential to lose auditors non-audit related fees.

Contingencies & Commitments

(Annual Report: Notes to the Financial Statements 30 & 31)

The contingencies and commitments seem to be small but in order to appear in the contingencies section the amounts must be able to be reasonably estimated.

Reasonable estimation can not be made with the outstanding litigation with which the company is involved.

Australian Competition and Consumer Commission Case:

The share price of RFG is related at least in part to the ongoing litigation between the Australian Competition and Consumer Commission (ACCC) and the company and its various entities.

The initial investigation by ACCC has dragged on for a long time.

They filed as plaintiffs claiming unconscionable conduct on behalf of RFG franchisees in the Federal Court of Australia on 15th December, 2020 (Number: NSD1333/2020 & Title: Australian Competition And Consumer Commission v Retail Food Group Limited ACN 106 840 082 & ORS).

There have been lots of delays and adjournments since. The respondent’s solicitors have contested ACCC’s claims at many turns and successfully delayed the final judgment.

Justice Katzmann in his latest judgment dated 19th August, 2022 ordered an adjournment which is the latest in a long series of adjournments.

Specifically;

He further ordered on 14th of September, 2022 that if the parties can’t agree by 27th September, 2022 on the composition of the franchises’sample under Order 4 of the judgment 19th August, 2022 then the Court Registrar will chose the sample.

ACCC administers the Franchising Code of Conduct which they state only applies to ‘franchising participants’.

There are some quite disturbing videos on YouTube.com on the experiences of some franchisees who had contracts with RFG.

Australia’s A Current Affair did a short documentary entitled Retail Food Group Investigation which was uploaded by a third party earlier this year.

The video includes a Part One and a Part Two.

The stories from some franchisees are heart-rending and although the company was asked for a response they declined.

It is difficult to try to place a potential settlement figure on this litigation as the outcome is so uncertain.

Michel’s Pattisserie Class Action:

The company recorded an impairment of $5.0m on this business unit in FY22.

Several franchisees have launched a class action against RFG. The court action had not been filed as at balance date.

The outcome of this potential case is uncertain and the company will defend the allegations strongly.

Possible Class Action:

The legal firm Phi Finney McDonald is advertising for franchisees to join a class action but no such action has yet been filed as of the FY22 balance date.

Related Party Transactions

There were no related party transactions of any real significance during FY22.

Directors & Senior Management

There are only three directors of the company and two of them are independent and non-executives.

This is a very small directorship for a company of this size. Does the company have the governance and expertise it needs with such a small directorship?

The directors have relatively small shareholdings in the company.

The position of executive chairman is a concern. Separating the chairman and CEO roles is best and Peter George seems to be doing both jobs although the CEO designation is not used.

It is notable that the CFO resigned during the year.

Performance Rights

Performance rights granted to senior staff carry and exercise price of $0.00 and are vested when performance criteria are met. The performance measure criteria include earnings before interest, tax, depreciation and amortisation (EBITDA).

Change of Balance Date

The company has changed its balance date from 2nd July in FY20 and FY21 to 1st July in FY22.

Often a change of the balance date is made in order to capture extra revenue or omit extra costs but it's not known if that's the case here.

Significant Accounting Policies

The individual components of the group have their accounts prepared in the functional currency being the dominant currency of the economic activities in which they engage.

At the end of each reporting period the non-Australian dollar amounts are recalculated into Australian dollars for the preparation of the consolidated accounts for the group.

Non-monetary items carried at fair value that are denominated in foreign currencies are retranslated at the rates prevailing at the date when the fair value was determined.

This is an interesting accounting policy because at balance date there could be significant differences in the original translation rate for the fair value items and the value determined by the translation rate at balance date for the other accounting items.

The exchange differences are recognised in the profit and loss statement except for some specific categories.

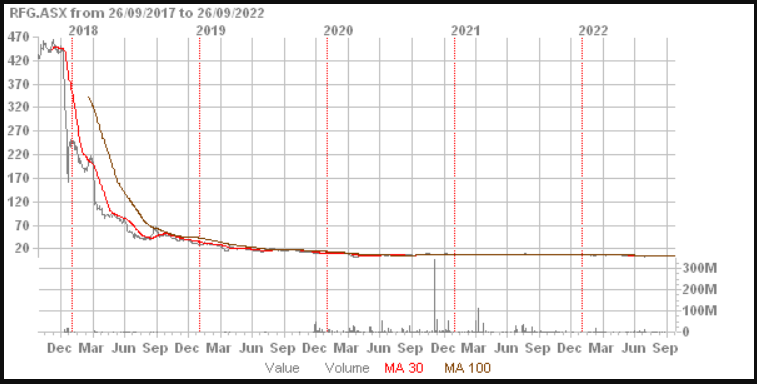

Trading History

Three Months:

Two Years:

Five Years:

The trading history of the company shows an extraordinary price collapse from more than $4.20 that occurred in late 2017.

In the first half of 2022 the stock found some stability around 6.5-7.0 cents region but then dropped to around 4.0 cents before rallying again for a period above 6.0 cents before falling and maintaining a range between 5.0 and 6.0 cents.

It has as yet, not shown any ability to consistently move up from its lows in the penny dreadful category.

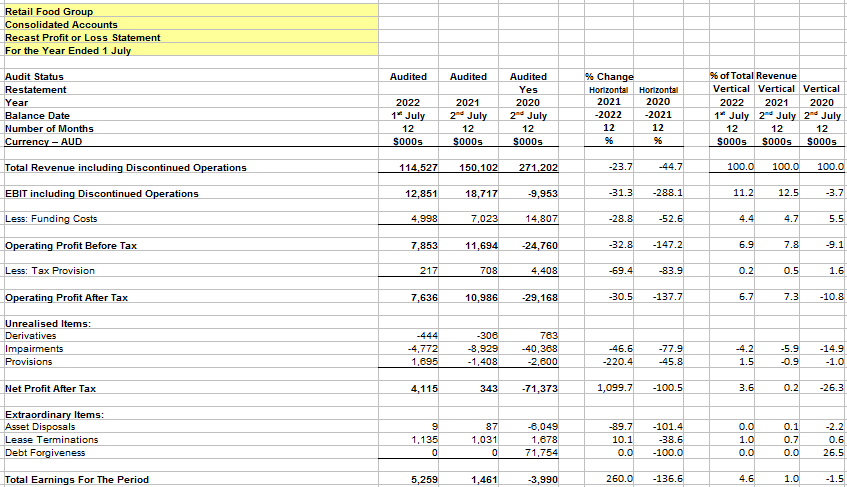

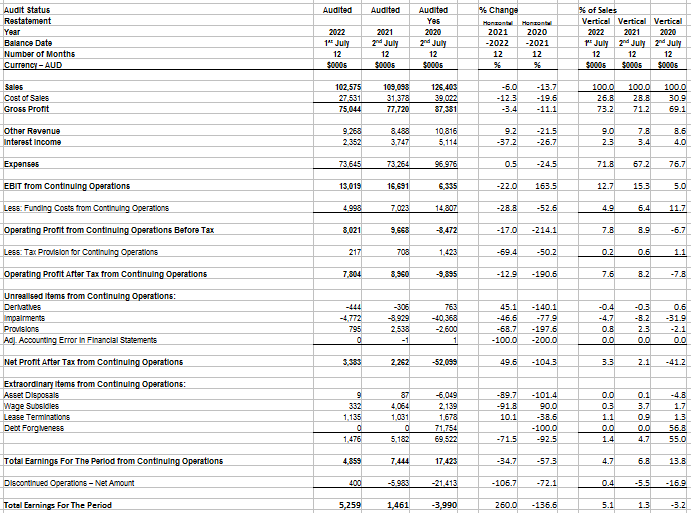

Recast Revenue Statement

The first interation in the recasting process is the simplest format. All revenue is aggregated in the total revenue item. This includes discontinued operations items and wage subsides. EBIT includes all expenses unless they are obviously unrealised or extraordinary.

This gives a clear and simple answer to the question; how much revenue was earned? Lower quality and some one-off items of revenue and expenditure are further down the statement.

This is the simplest form of presentation before the separation of additional one-off items and other recasting changes are made.

Iteration 1:

In the second iteration the discontinued operations are separated out from continuing operations and the wage subsidies recategorised from total revenue and itemised as extraordinaries.

Iteration 2:

The gross margin has improved in both FY21 and FY22 at 71.2% and 73.2 % respectively which is encouraging. The gross margins are also high.

It is disappointing that sales have declined and in the latest period were down 6.0%. This was more than compensated for by a decrease in cost of goods sold which reduced by 12.3%.

EBIT from continuing activities was down a very significant 22.0% to $13.0m for the FY22 year.

This is offset by a reduction in funding costs as the company’s debt declines.

Total earnings from continuing operations which is often called underlying total earnings were down by 34.7% to $4.9m mostly as a result of falling government wage subsidies.

Discontinued operations didn’t impact the current period nearly as much as the prior period and the company was able to post a 260.0% increase in total earnings from all sources to $5.3m.

In FY23 the total earnings from continuing operations in FY22 (which declined to $4.9m) are obviously the most relevant.

Wage Subsides:

Government wage subsidies, both domestic and international had previously been netted off against employee benefits expenses and then allocated to different expense items.

The wage subsidies were taken out in the analysis and added to Iteration 1 total revenue, then removed from revenue to extraordinaries in Iteration 2.

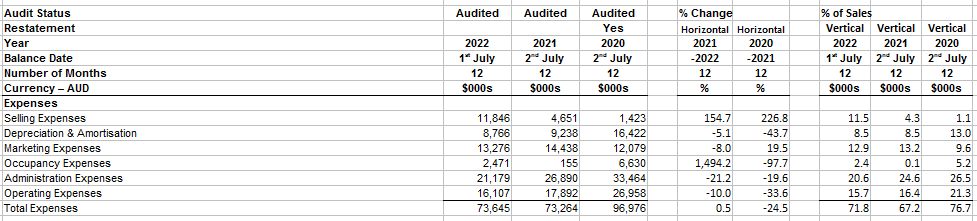

Expenses:

Occupancy expenses and selling expenses have increased dramatically in FY22 but it’s not clear if this is because expenses have been recategorised. This may be the case as overall expenses remain fairly similar in FY21 and FY22.

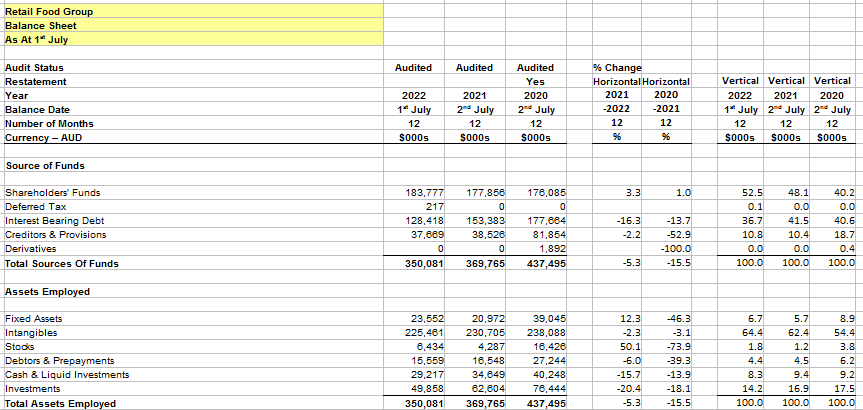

Recast Balance Sheet

The most obvious issue is the very large percentage of intangibles to total assets of 64.4% in FY22. Without these intangibles the company would meet one of the criteria for insolvency.

The intangibles are so large they are greater than the shareholders’ funds.

Intangibles:

(Annual Report: Note 14.8: Goodwill)

“The valuation technique adopted was an income-based approach by using a discounted cash-flow model”.

As interest rates increase in Australia and elsewhere the assumptions that underly the calculations of intangible asset values need to be reassessed.

The discount rates of future cash flows upon which goodwill and brand systems intangible assets’ fair values are calculated will need to increase and this leads to decreases in the carrying amounts for goodwill and brand systems intangible assets.

In FY22, the pre-tax discounts rates for these items ranged between 12.08% and 13.09% for operating segments goodwill and 11.80% to 12.0% for brand systems intangibles.

The trigger discount rate, for example, for activating impairment in the Di Bella Coffee Brand System is 13.9%. Its FY22 discount rate was 13.19%. With current and coming big interest rate rises from central banks it’s safe to say that impairments will be triggered again over the next year or two.

These will significantly impact profits over the next couple of years if the impairments are run through the revenue statement.

Long term growth rates in the discount model for imapirment calculations ranged between 2.2% and 2.5% for operating segments goodwill and 0.5% (Michel’s Patisserie Brand System) and 2.5% for the brand systems’ intangible assets.

The growth rates seem reasonable given they are nominal and do not take into account inflation rates which are currently higher than they are.

Debt:

The debt in the company is not significant compared to total assets and all bank covenants’ conditions are met as of the FY22 balance date.

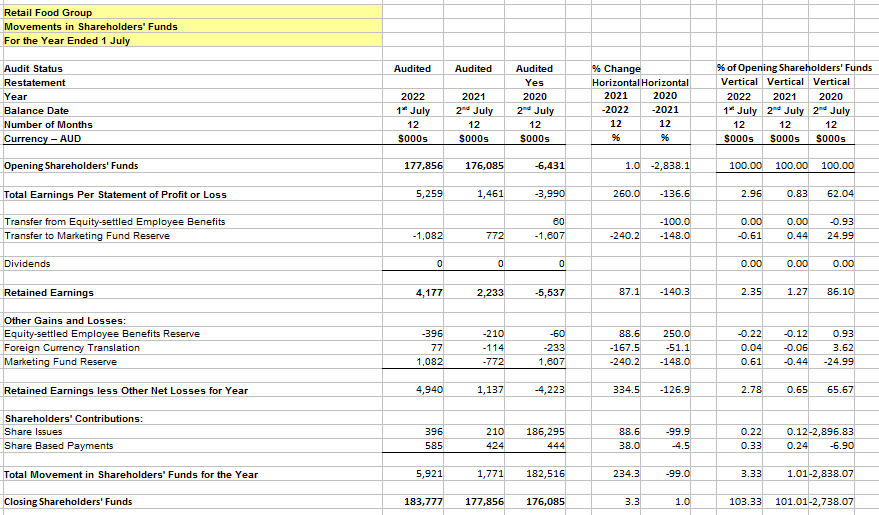

Recast Movements In Equity

Shareholders’ funds increased by 3.3% in FY22 YoY. There were few significant events such as the ones that occurred in previous years such as the massive share issue in FY20.

Recast Cash Flow Statement

The cash flow statement includes discontinued operations.

Net operating cash flow has increased over the last three years which is a good sign. In fact it was up by a solid 39.4% in FY22.

The surplus cash flow from operations was used for small investing items and the bulk plus some extra cash was used to retired interest bearing debt. The closing cash balance as a result was 15.7% down on the prior year at $29.2m which is still a healthy bank balance.

Ratio Analysis

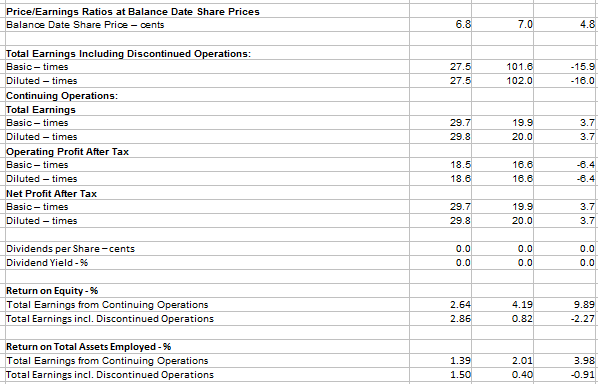

Funding cost cover is a solid if not spectacular 2.6 times both with and without discontinued operations included.

Basic and diluted total earnings from continuing operations are both 0.23 cents per share which results in P/E ratios of 27.9 and 27.8 respectively.

Return on equity from continuing operations was a paltry 2.64% based on total earnings. This is less than current term bank deposit rates.

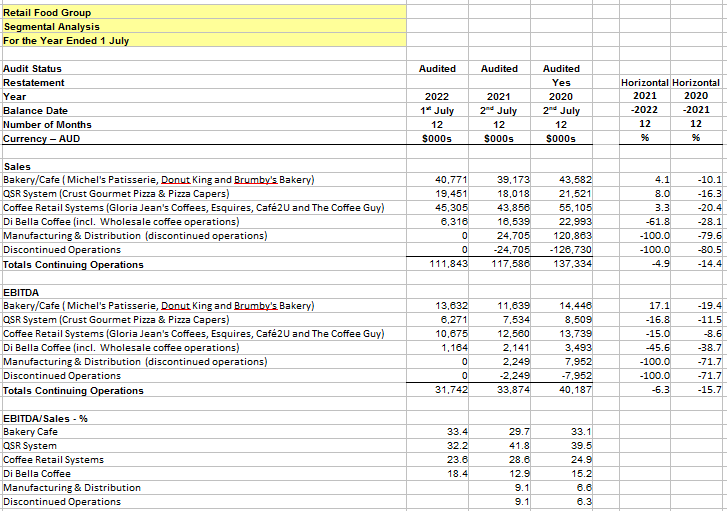

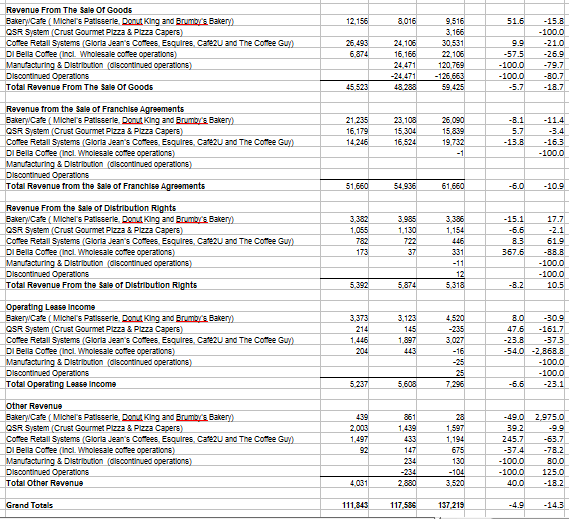

Segmental Analysis

Segmental Revenue Streams by Business:

Segmental Revenue Streams by Activity:

There is a lack of information in the annual report which could help in analysing the various segments of RFG’s businesses.

There were small sales increases in the bakery/cafe, QSR systems and coffee retail systems while there was a large fall in Di Bella coffee sales.

EBITDA, a measure that should be looked on sceptically but which is the only return metric available for segments provided by the company fell across the board except for the bakery/cafe business.

Sales by revenue activity are also down across the board.

Summary

The company’s future is still not certain and the balance sheet relies on massive intangible asset valuations for its financial health. The equity ratio based on these intangibles is a healthy 52.5% but it must be born in mind that intangibles exceed the value of shareholders’ funds.

The situation could change quickly for the company if things went poorly in the general economy in the light of rapidly rising interest rates which will no doubt impacted intangible valuations in the current financial year ended 2023.

Will these possible impairments appear in the next year’s revenue statement and if so, will they wipe out the year’s profit?

How reliable is the audit opinion given that income from work outside the audit and review engagement now exceeds the audit and review fees? This is not to say that the auditors are in any way dishonest but that on questions of judgement opinions can vary and be supported by good arguments.

The governance question is one that is important. The directorship is small (three people) and there is no separation between the chairman and what is normally called the CEO role. This is concerning and too much control may rest with one individual, Peter George.

On the positive side, the company so far has survived the cataclysm of Covid-19 and other major business problems over the last few years. This has been no mean achievement given what has happened.

There is some evidence that things are improving as the economy recovers to some degree from the Covid-19 madness. But it should be borne in mind that Australian authorities overreacted to it and that these ridiculous government approaches may again occur.

The overhanging potential class actions and ACCC action are a weight on the company that reflect times when the management acted poorly. Hopefully, those days are long gone.

However, it’s concerning that no settlement/judgement has been reached in the ACCC case as a result of the company’s lawyers continually dragging out the legal jousting.

With low debt (subject to reservations on intangibles values) the company could surely come to some agreement with the ACCC, the Federal Court and the class action participants. It’s disappointing that these issues are still hanging over the business and its (most likely) share price.

RFG has anaemic EPSs and high P/E ratios even at these low share price levels. The total earnings from continuing operations fell for FY22 and this is concerning in the light of an end to wage subsidies and possible future impairments to intangibles of individual business units.

The net profit after tax for FY22 also fell even after a lower tax charge.

With the very low share price the question might be asked whether a share consolidation could be a good option in the near future.

There seems to be no movement in the share price in recent times that would indicate significant enthusiasm for the stock. Any improvement in the share price is subsequently reversed.