Basic Analysis: Retail Food Group (RFG.ASX)

Annual Accounts to 2 July, 2021

Photo by Tyler Nix on Unsplash

Key Points

Awaiting outcome of ACCC litigation and resolution of potential franchisee class actions

Improving profitability

Low debt

High intangibles

Acceptable operating cash flows

Negative NTA per share

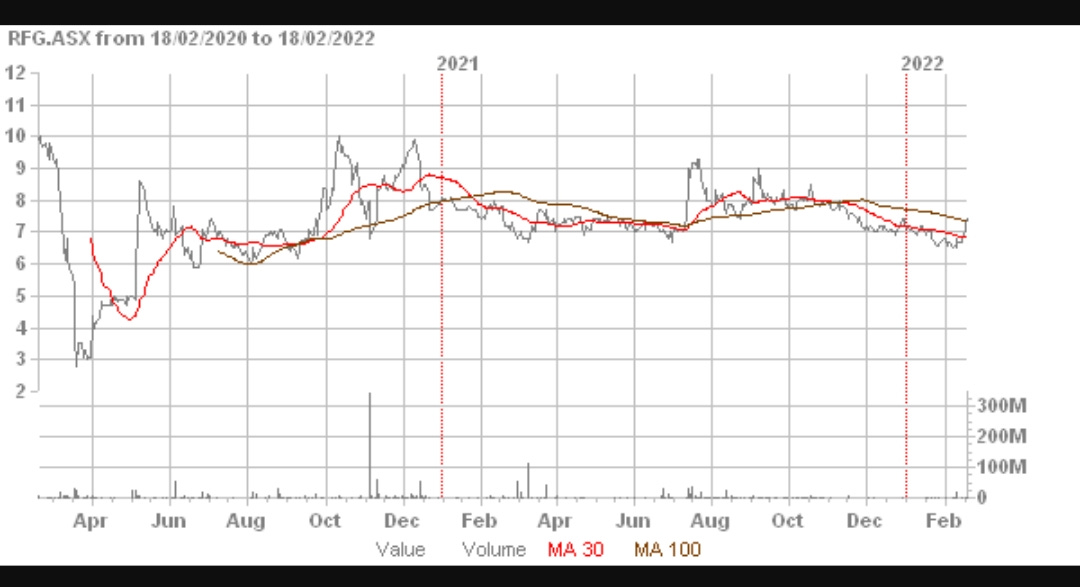

Source: Direct Broking

Note: All figures in AUD.

Recast Revenue Statement

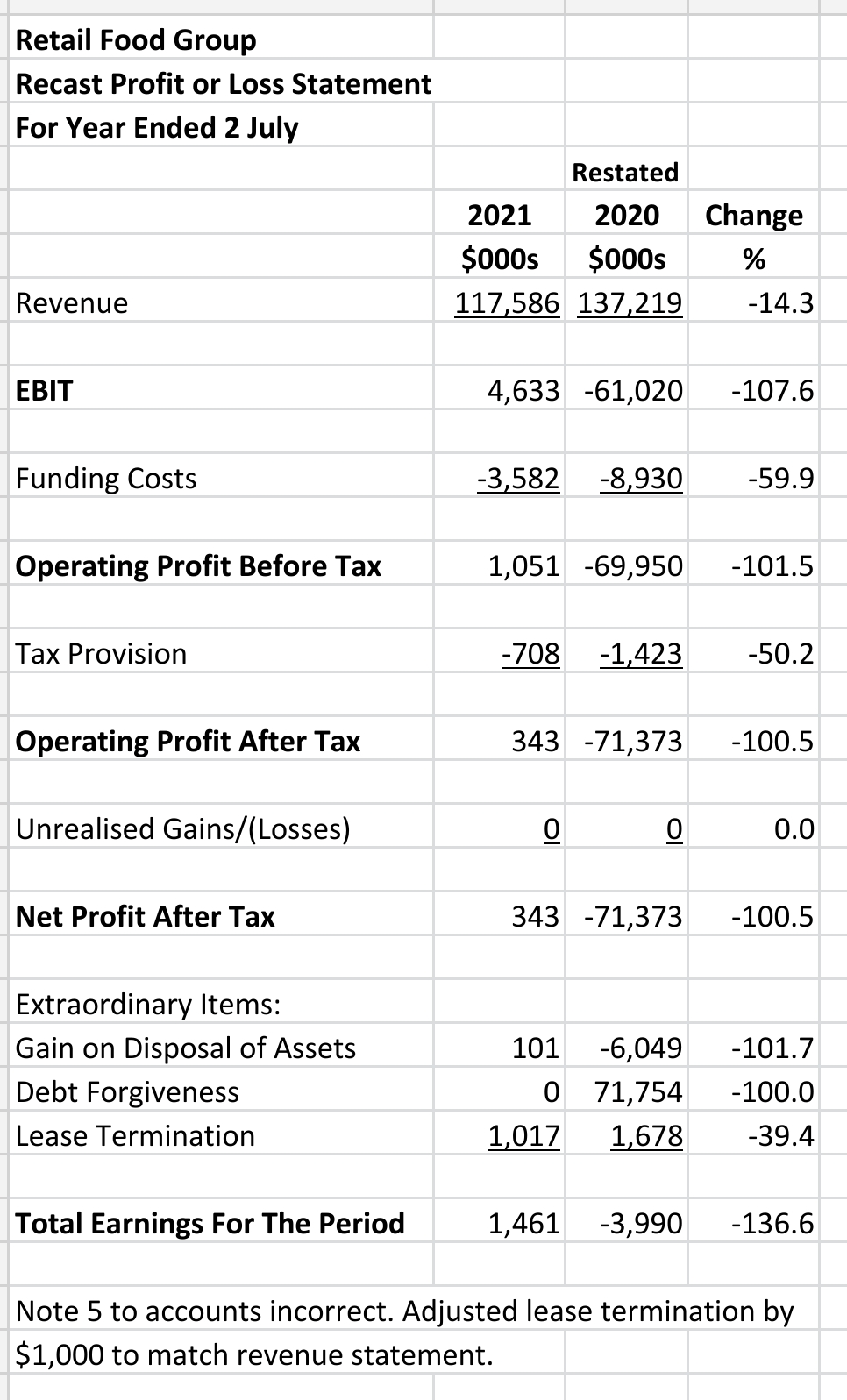

The company discontinued some operations in the current period and the costs of doing so are recorded in arriving at the EBIT figure.

Revenue was down 14.3% to $117.6 mn while there was an impressive turn around in EBIT to $4.6 mn which was enough to cover total funding costs in the year.

Profit figures were low with total earnings for the period of $1.5 mn which was a an improvement in the prior year which relied on debt forgiveness to achieve its total earnings of -$4.0 mn.

The prior period relied on extraordinary items to reduce a massive loss of $71.4 in net profit after tax.

Recast Balance Sheet

Horizontal Analysis:

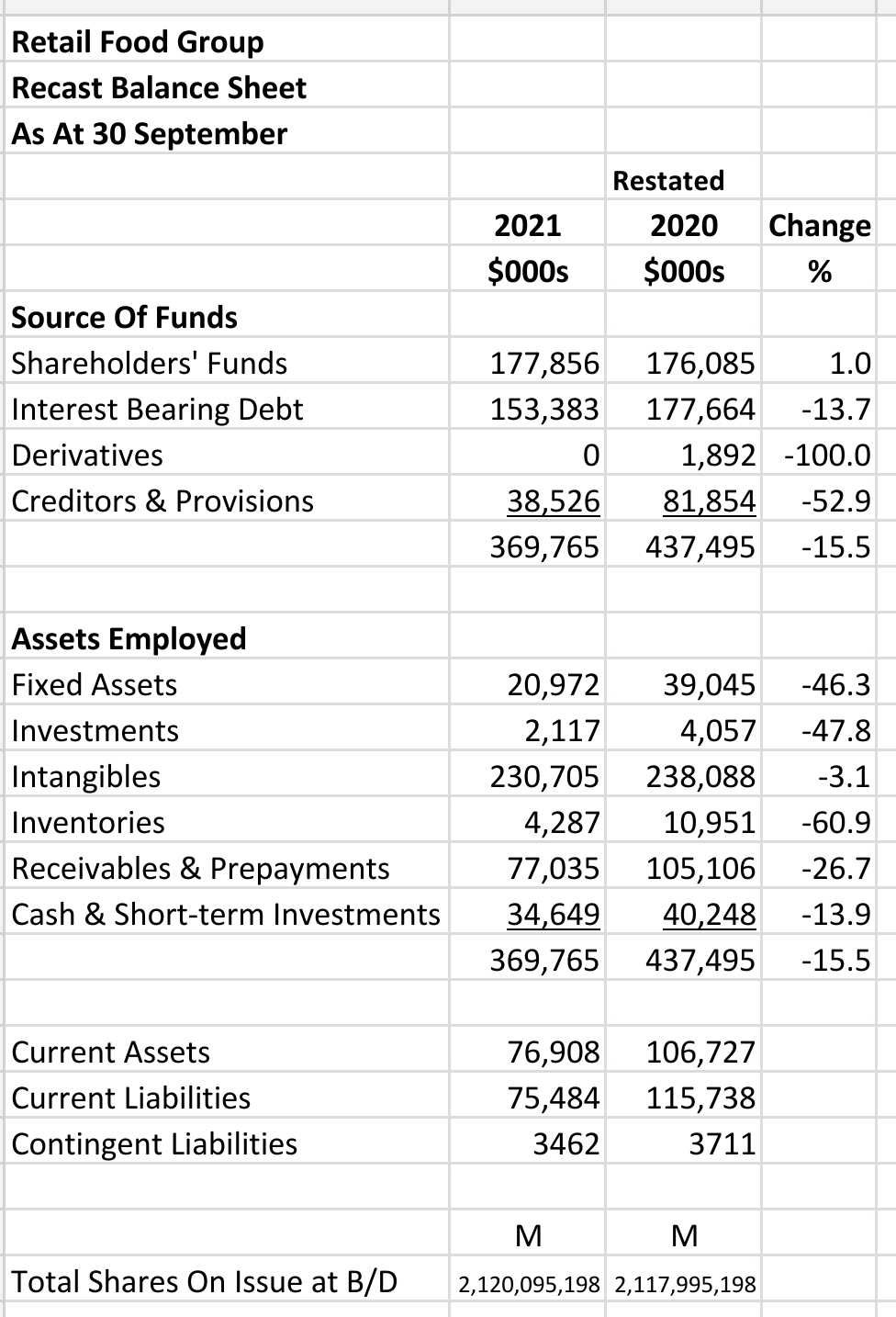

Total assets decreased 15.5% to $369.8 mn in the current period due to restructuring while shareholders' funds was little changed.

Vertical Analysis:

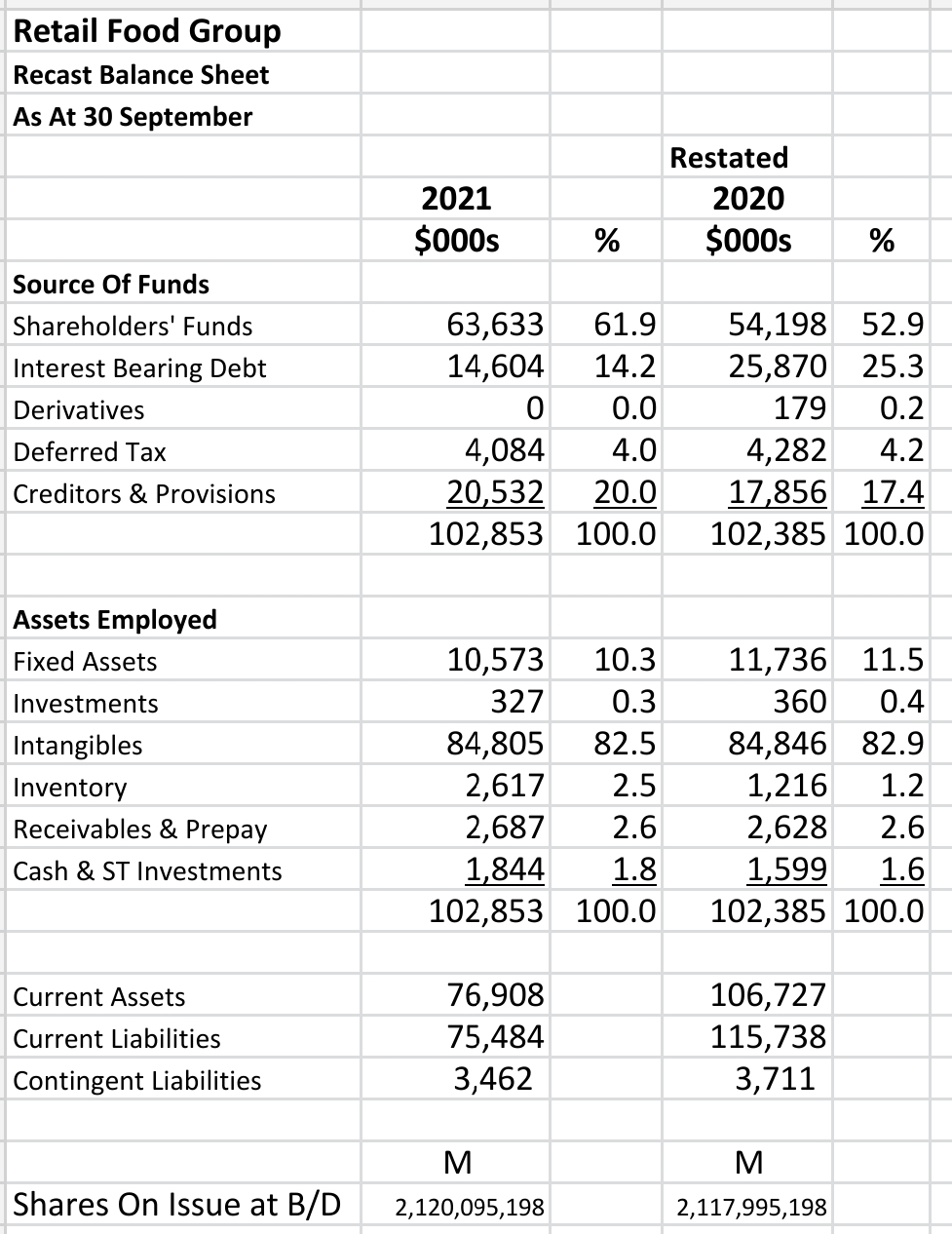

The most obvious feature if the balance sheet is the very large levels of intangibles which dwarf every other item in total assets. They represent 82.5% of the assets employed in the company.

The accuracy of the intangibles' valuations is critical to the quality of the balance sheet.

Recast Statement of Movements in Shareholders' Equity

A large share issue in the prior period of $183.2 mn brought the company back from technical insolvency . The opening shareholders' funds in the current period was positive as a consequence at $176.0 mn.

Recast Cash Flow Statement

Operating cash flow was strongly positive in the current period at $11.1 mn.

$18.4 mn of interest bearing debt was retired (after expenses).

The company ended the current period with a cash balance of $34.6 mn which was 13.9% down on the start of the period.

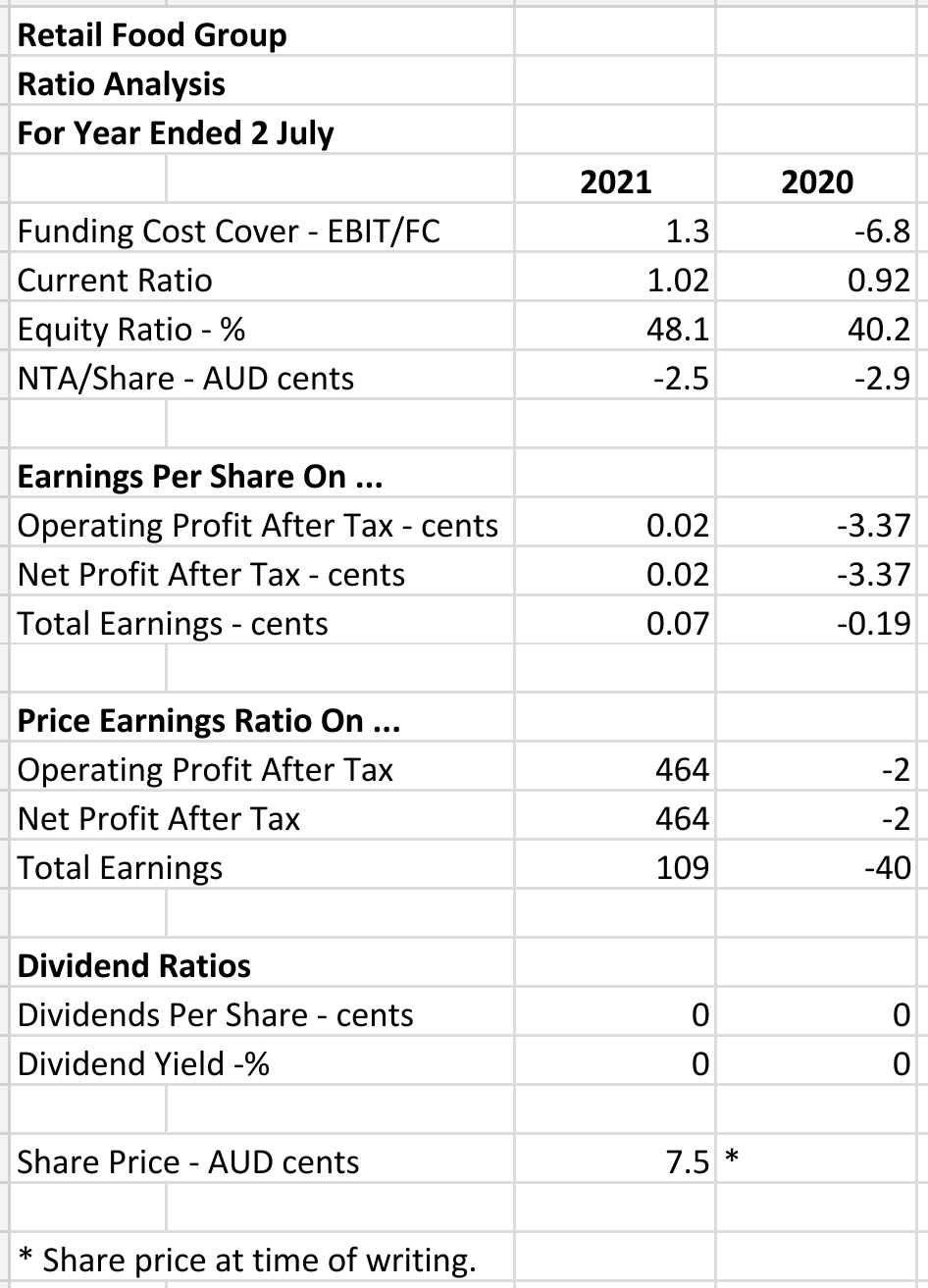

Ratio Analysis

The company had negligible earnings per share mainly because there are so many shares on issue. A consolidation of shares would probably be advisable.

The price earnings ratios were extremely high at all levels of profit.

The equity ratio is 48.1% which is acceptable for a company in these industries. However, it is based on extremely high intangible valuations so must be considered with that in mind.

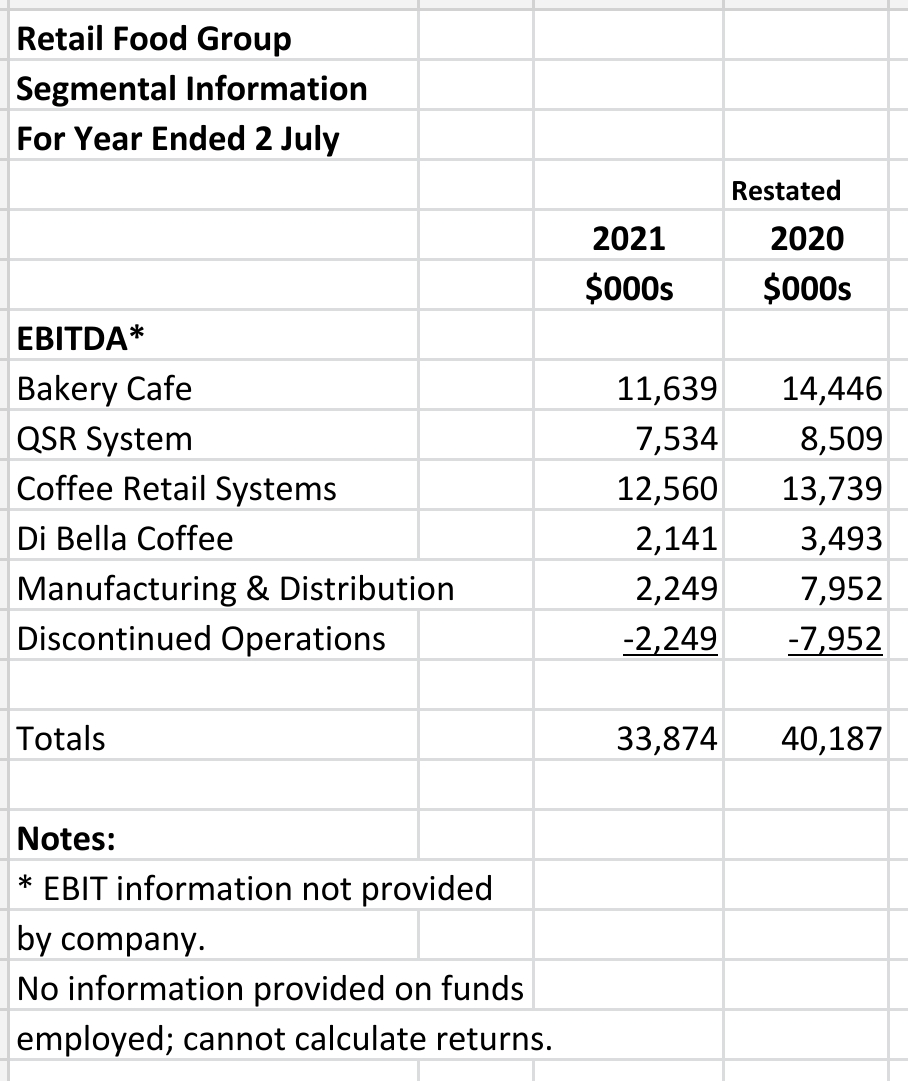

Segmental Analysis

The company provides very little information for any segmental.analysis.

The bakery cafe and coffee retail systems provide the highest EBITDA contributions but returns cannot be calculated.

Summary

The company is in the process of turning around its bad fortunes. It has shed non-core businesses, issue equity and retired debt in its efforts to become successful.

Unfortunately, there are a number of legal concerns outstanding which cannot be accurately quantified.

Very good write up. I do believe with the backing from Washington H Soul Pattinson, that will provide better transparency and governance that will keep the company in check. On top of that, SOL is able to provide some guidance that will help RFG to hit those objectives over a certain period of time. This could be one of the hidden gems that could be a 1 - 2x bagger stock if executed correctly. We will see a potential probability of seeing those legal charges to be resolved and hitting better margins during xmas period as part of the catalyst to bump the share price to go higher.