Basic Analysis: Victoria PLC (VCP.LSE)

Financial Statements for 53 Weeks Ended 3 April, 2022 (Two Years)

Note:

All figures are in UK£ unless otherwise stated.

Industry

Carpet & Flooring

Listed Securities

LSE: Ordinary Shares

Data

Basic accounts data for this company can be accessed here:

Key Points

Poor share price

Low profitability

Positive cash flow from operations

Expanding balance sheet through acquisitions funded by debt

Negative net tangible assets

Strong cash position

No dividend

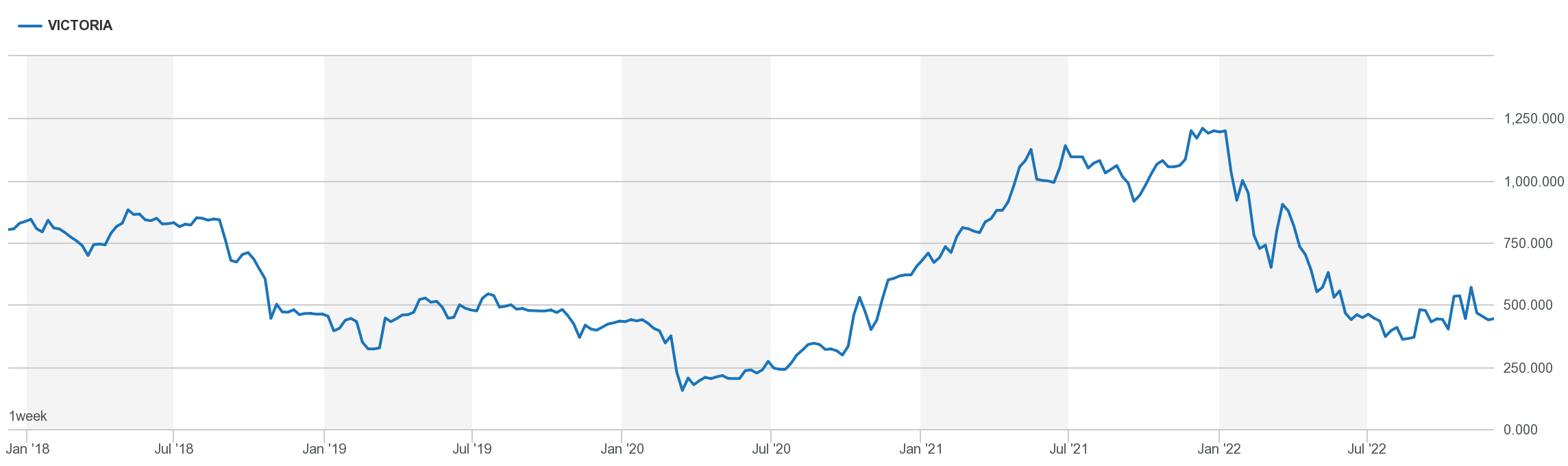

Trading History

Source: Londonstockexchange.com

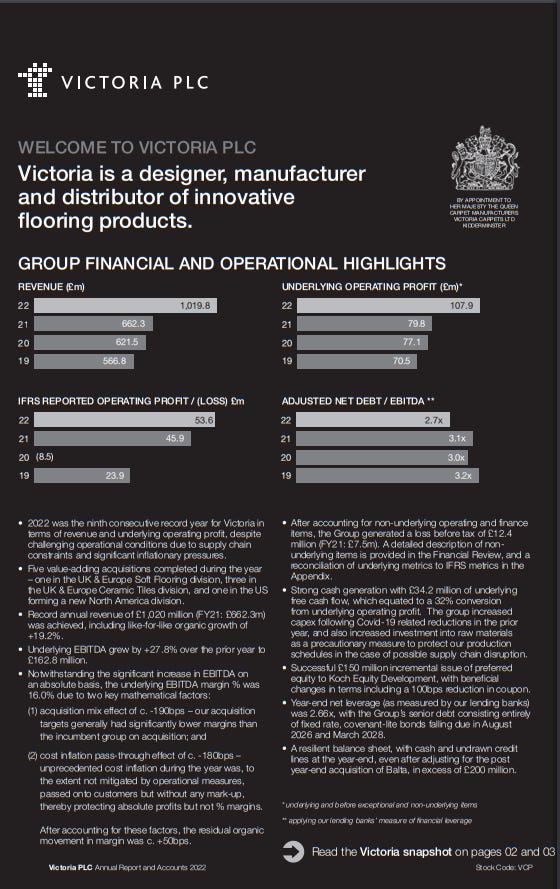

Financial Highlights

Source: Victoria Carpet, Annual Report and Accounts 2022

Overview

Victoria PLC (VCP) has a New Zealand connection. The chairman and also significant shareholder, Geoff Wilding is from New Zealand.

Wilding was involved in a number of listed and unlisted New Zealand companies before his move to the UK.

These companies included Commsoft, a listed entity which traded on the NZX around the beginning of this century and ran into trouble in the Dot Com Crash.

He was then involved in building Pacific Print Group which rolled-up smaller private printing companies and eventually became Geon.

This company later (after Wilding left) ran into trouble and was liquidated in the late naughties.

The rationale of this business strategy was that large public companies sell at significantly higher P/E (price earnings) ratios than private companies.

Value can therefore be created by aggregating small companies into a bigger one. And if synergies can be obtained then all the better.

This strategy means that the holding company executives do not need vast knowledge of the nuts and bolts of the operational units (at least in theory).

There was also some involvement with a roll-up of carpet franchises in New Zealand which traded under the Carpet Court brand and some other private companies.

The last company was promoted by Rodney Martin, an Auckland entrepreneur and business partner of Geoff Wilding's.

Geoff Wilding and Rodney Martin left New Zealand after Carpet Court was sold under lender direction.

The former settled in England and became involved with VCP where he became chairman after a fight with the board of directors.

Martin retained an involvement and now sources acquisitions through his Malta-based private company which is called Obsidian Capital Partners.

VCP was established in 1895 as a carpet manufacturer.

Under the chairmanship of Geoff Wilding the company has been rolling up (pun intended) private flooring businesses from around Europe, North America and Australia using the same basic strategy that was used with Pacific Print Group and Carpet Court except on a larger scale.

VCP is now an entity which has total revenues of over £1 bn in FY22.

Wilding arranged a performance-based derivative package with the company which has seen his ownership in the company increase over the last few years.

The business has been very rewarding for Mr Wilding. He now controls close to 20% and has recently purchased the superyacht Resilience.

Source: yachtcharterfleet.com

The superyacht is available for charter at over Euro 320,000 per week so it may make independent financial sense on that basis.

The share price of VCP reached a high of over £12 but began its slide around late 2021 to around £4.40 where it currently trades.

A Note On The Accounts

The accounts for this company are complex and made even more difficult with changing balance dates. Also, there are errors such as a big one in the prior year’s financing cash flow in the cash flow statement.

The use of EBITDA and underlying earnings is pervasive. Separating non-underlying earnings strangely (lol!) always improves the position of the company especially the revenue statement.

For a number of reasons EBITDA is a relatively poor metric for judging a company’s performance but has value with regard to comparing companies. EBIT is used in this article.

Please note that the periods covered are not identical; one for 52 and one for 53 weeks.

Although the half year report for the interim period to 1st October, 2022 has now been published it will be reviewed in a later article. Background to the company obtained by reviewing the annual report for 2022 will be useful and this is the reason an overview is given here at this late date.

VCP is the first LSE, or for that matter any European company reviewed and the format of the accounts differs in minor ways from Australian and New Zealand companies.

Recast Revenue Statement

The revenue for the year was up 54.0% to £1,019.8m producing a gross profit up 51.9% to £356.8m.

The gross margin declined from 35.5% to 35.0% in the pcp.

EBIT was £107.5m compared to £79.7m in the pcp. Operating profit after tax was £41.5m while net profit after tax was only £1.3m.

Total earnings were a loss of £12.4m compared to a profit of £2.8m in the pcp.

Negative goodwill on acquisition contributed £6.1m in profit to the revenue statement. Negative goodwill on acquisition occurs where a company was acquired for less than its book value or fair value.

This negative goodwill is a problem because it could be argued that the fair value of the acquiree is the price paid because that is what the business sold for in the market.

But the legitimacy of running the negative goodwill through the revenue statement must be questioned in terms of its quality of earnings despite the accounting standards concerned.

To that end negative goodwill on acquisition is included in the recast revenue statement under unrealised items denoting this lower revenue quality.

Hidden away under the balance sheet on page 63 of the Annual Report is the statement, “The loss of the Company for the year determined in accordance with the Companies Act 2006 was £30.8m (2021: loss of £30.9m)”.

Why was this statement not on the revenue statement page? The Companies Act 2006 is a voluminous tome and at this stage the reasons for the differences are not investigated.

Recast Balance Sheet

Shareholders’ funds declined during the latest period to £202.6m producing, even with the large level of intangibles on the balance sheet an anaemic equity ratio of just 12.2% which is down on the pcp’s 15.4%.

This kind of equity ratio is too low for this type of company and is more often seen in the banking or finance industries.

Subtracting the intangibles amount results in negative net tangible assets of -£301.7m at balance date. This is significantly lower than the pcp’s -£180.8m.

Interest bearing debt has soared by 22.6% to £1,031.1m as the company’s acquistions have continued apace in FY22.

The large intangibles item of £504.3m represents 29.6% of total assets.

Recast Movements in Shareholders' Equity

Even though the company does not pay dividends on its ordinary shares the shareholders’ funds continued to decline in the FY22 although not by as much as the decline in FY21.

Recast Cash Flow Statement

The recast cash flow presented by the company used the indirect method which is used in the UK but usually appears in the notes to the accounts in New Zealand where the direct method is favoured.

There is a significant error in the calculation of financing cash flow in the prior period which is highlighted in red in the data download at the top of the article.

Moving lease liabilities into operating cash flow using this method changes the operating cash flow to £53.1m.

The company produced positive operating cash flow and together with positive financing cash flow used the funds mainly for acquisitions.

But there was still a reduction of cash of £90.1m and the year ended with a cash balance of £258.0m (after overdrafts were taken into account).

Ratio Analysis

The company has poor funding cost cover of 1.6 times and NTA/share of -£2.58.

Its basic EPS is -10.6 pence based on total earnings for the FY22 period while its diluted EPS based on total earnings for the period is -9.0 pence. Both of these figures are way down on the pcp where the EPSs were 2.3 pence and 2.2 pence respectively.

Based on the profit calculated under the Companies Act 2006 the EPSs were -26.4 pence for basic and -22.3 pence per share for diluted which are obviously very poor results.

Outside of EBIT the returns on shareholders’ funds were minimal and for FY22 the return on shareholders’ funds for total earnings were an abyssmal -6.1%.

Net Debt/EBITDA was 3.9 times while EBITDA was £195.1m.

Since the prior period’s balance date the market capitalisation of the company has plummeted from £1,332.1m to £523.5m at the FY22 balance date. This represents a total capital loss for ordinary shareholders of £808.6m or 60.7% between balance dates.

Segmental Analysis

Ceramic Tiles were the worst performer returning an operating profit of 4.5% against its equity while UK & Europe Soft Flooring was the best performer returning 16.9% on the same metric. Australia was not too far behind at 15.6%.

It’s notable that the worst performing segment, Ceramic Tiles, had the largest share of net assets (equity) of £491.4 apportioned to it.

Summary

Victoria PLC was a sleepy company until a New Zealand entrepreneur reinvented it through acquisitions and in the process created one of the largest flooring concerns in Europe.

However, the share price has done poorly in recent times and there are whispers that some significant short positions have been made previously in the stock.

The company has grown very quickly and provided great returns for those that got in around the time of Wilding’s initial involvement.

But rolling-up flooring companies on this scale does not seem to be producing good profits and the leverage is very high.

The document on the Abingdon Case Study available on the company’s website was an effort to assure participants that VCP could add value and provide synergy through acquisitions and not just bolt them on to an existing monolith.

The company has positive operating cash flow, at least as far as can been seen in this relatively cursory examination. The use of negative goodwill on acquisition to bolster profits is somewhat of a concern. It was material in FY22 but not overly so.

The interim accounts to 1st October, 2022 will be covered in the next few weeks. As stated above this was a brief examination of previous accounts to see the ‘lie of the land’.

Yes, and the share price has dropped dramatically. Wonder if the company survive.

Multiple red flags around Wilding and Co