Update: Retail Food Group (RFG.ASX)

Interim Accounts to 30th December, 2022 (Three periods)

Note: All amounts in AU$ unless otherwise stated.

Overview

Retail Food Group (RFG) has been on a rocky road to the possibility of recovery over the last few years. It’s recently decided to do capital raisings of debt and equity.

It also recently announced its results for HY23, the period ending 30th December, 2022. This announcement was made on the 28.2.23.

Three days later, on 3.3.23, it announced the debt and equity capital raisings.

The equity raisings consist of two parts. Firstly, $24,900k via a share placement to sophisticated and institutional investors at an offer price of $0.08 per share for which commitments have been received. Secondly, a share purchase plan to raise approximately $2,500k, which allows existing eligible shareholders to participate.

The debt raising is a new $20,00k facility with Washington H. Soul Pattinson and Company Limited.

This total capital raising of around $47,000k compares with existing total assets of $356,473k and will just bring the balance sheet back into slightly positive net tangible assets.

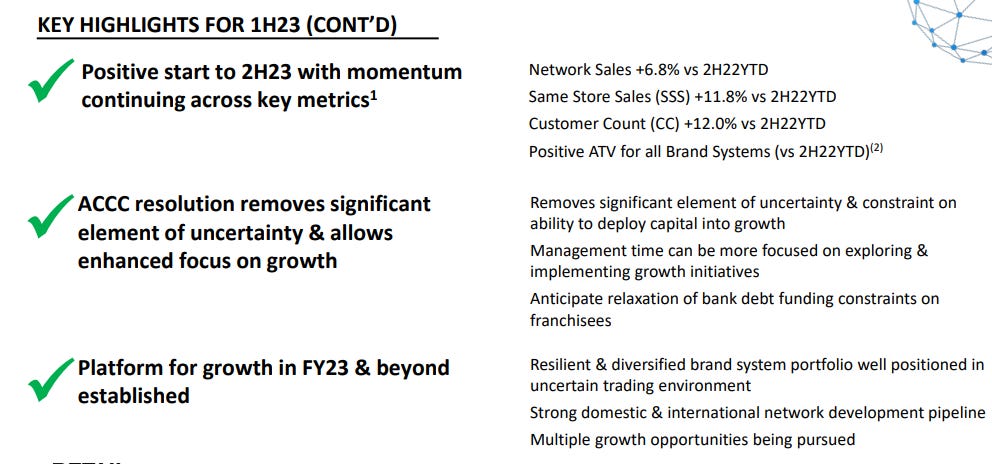

Company Stated Highlights

Source: RFG 1H23 Results Presentation

When a company highlights an EBITDA figure which shows improvement it’s often masking more important financial information that doesn’t convey as optimistic a picture.

Companies are in business to make profit not EBITDA and leaving out depreciation and amortisation is inaccurate and misleading.

In the images above the company highlights a 47.4% increase in EBITDA but its profits are falling.

Same store sales (SSS) are also not profit and nor are customer count (CC) or average transaction value (ATV).

Trading History

ASX:

Source: Direct Broking

Source: Direct Broking

The company’s trading recently is interesting and was addressed in this Tradeshot.

Key Points

No dividend

Large ACCC settlement of $8,035k paid

Large increases in both trade & other payables and also provisions - slow paying?

Leased asset impairments reversal of $5,027k

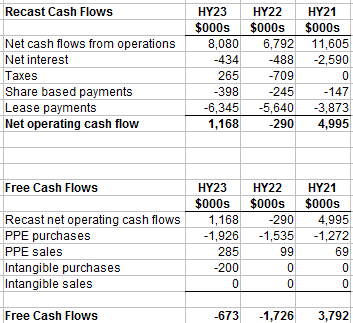

Positive recast operating cash flow of $1,168k but negative free cash flow of $673k

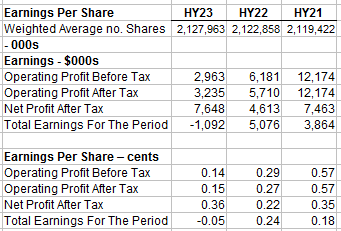

Operating profit after tax is $3,235k

Total earnings were -$1,092k

Negative tangible assets of $52,380k and it will be negative after the capital raisings

Contingent Liabilities

The company paid its ACCC settlement during HY23.

The outstanding matter of Michel’s Patisserie Class Action is still being litigated. The outcome of this litigation is uncertain according to the notes to the interim accounts.

Recast Revenue Statement

The gross profit figures include multiple sources if revenue so the actual gross profit figures may be distorted. Some types of revenue have no or minimal COGS such as franchise sales.

The company increased revenue from contracts with customers by 14.4% but lost $1,092k in HY23.

The company had to pay an ACCC settlement of $8,035k during the period which impacted profit significantly.

This was largely offset with a $5,027k reversal of previous impairments to leased assets.

Often companies will hold back impairment reversals for a time when they can smooth profits as may be the case here.

It was obviously ‘highly fortuitous’, because it reduced the impact of the ACCC settlement significantly.

The EPS figures cover just a half year so P/E ratios can’t be determined but the earnings in HY23 were low on a per share basis.

The most relevant figures in the revenue statement are EBIT and operating profit after tax.

EBIT, which shows the company's ability to service it's debt, was down 35.4% on the pcp. The most recent pcp had been down 43.9% on its pcp.

HY23 operating profit after tax was down 43.3% at $3.24m on the pcp following on from a 53.1% decline on the pcp's own pcp.

The latter measure is close to what analysts call underlying earnings.

The fact that there was a tax credit rather than tax payment indicates the company over some period is not making taxable profits.

Balance Sheet

The balance sheet is stacked with intangibles and if these are removed the shareholders funds are negative.

Trade & other payables increased a lot and were $17.4m at balance date on HY23 while they were only $10.7m at balance date in the pcp. This is a 62.6% increase on a revenue on contracts with customers increase of just 14.4% on the pcp.

The company may be slowing down the payment of its creditors. Inventories have also fallen compared to the pcp’s balance date.

Most of the company's borrowings at balance date in HY23 were current (repayable within 12 months) which probably was why the debt raising was required.

Either their lender(s) didn't want to roll the current portion on its maturity or the company could achieve better terms elsewhere.

Movements in Equity

Total shareholders' funds declined slightly during the HY23 interim period from $183,777k to $183,192k.

Cash Flow Statement

There was $398k of equity settled share based payments which are non-cash. However, when they are included in operating cash flows and added back to financing cash flows (which cancel each other out in terms of net cash) a true picture of the operating cash flows situation can be determined.

Additionally, the lease payments appearing in financing cash flows are moved to operating cash flow.

There are no dividends but if there were they would need to be moved to operating cash flows as, like interest payments which appear in operating cash flow under most GAAP, they are a cost of capital.

The difference between interest payments and dividend payments is only that the latter are discretionary.

The company’s repayment of borrowings of $5,000k accounted for most of the $5,163k change in cash for the HY23 period.

An indirect cash flow statement would have been useful for extra information but this reconciliation is not required under listing rules for interim periods in the company's domicile.

Free cash flow was -$673k but an improvement on the pcp. Free cash flows are calculated as recast operating cash flows less net PPE and net intangible receipts and payments.

Segments

Segmental information provided in the interim accounts is largely useless as EBIT and net segmental profit figures are not provided.

All that can be said is that revenue is up in Bakery/Café, QSR Systems and Coffee Retail Systems while it is down in Di Bella Coffee.

The one figure that stands out is the restructuring & provisioning figure for HY23 of -$6,753k which doesn’t seem to pop up in the revenue statement where the figure was -$470k. Odd indeed.

Summary

The company trumpeted it’s results with EBITDA, CC and SSS information.

However, an inspection of more relevant metrics such as EBIT and operating profit after tax shows a different situation.

It's results are poor, its balance sheet is of suspect quality given the size of the intangibles and the trend in results, at least over the interim periods discussed is down.

Recognising the company's current weaknesses, the directors decided to raise both debt and equity although not in large amounts compared to total assets.

The equity portions of the capital raisings are at 8.0 cents and this is above the current market price of 6.7 cents.

Nevertheless commitments have been made at the higher price for $24,900k but the other equity amount of $2,500k may be difficult for the company to achieve.